- آموزش امواج رابرت بالان الیوت

- cryptocurrency بعدی برای منفجر شدن در سال 2022

- با افزایش سهم لوکس ، براساس آخرین داده های قیمت معاملات Kelley Blue Book ، قیمت های جدید در ماه نوامبر رکورد بالایی دارد

- FP Markets Account Demo: چگونه می توان از آن با تجارت استفاده کرد؟- یک آموزش سریع

- سبد سرمایه گذاری خود را بسازید

- 15 قانون معاملاتی ویکتور اسپراندو برای جلوگیری از اشتباه و دستیابی به بازدهی چشمگیر

- نحوه خرید سهام Google: سرمایه گذاری در سهام غول فناوری

- رالی بزرگ Smallcap. 5 رهبر و عقب مانده برتر.

- پنج اشتباه بزرگ از سرمایه گذاران "Do-It-Yourour"

- مسیرهای عصبی

آخرین مطالب

امکانات وب

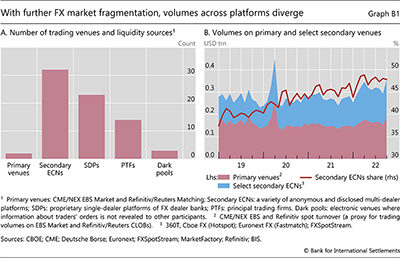

فعالیت معاملاتی در بازارهای FX در طیف وسیعی از مکان ها و ارائه دهندگان نقدینگی تکه تکه می شود (کمیته بازارها (2018)). Before the tu of the millennium, the FX market was a "plain vanilla" OTC market, with trading dominated by major dealers. While still retaining its OTC structure, a multitude of other venues and providers has emerged since then (see eg Chaboud et al (2022)).

Before the tu of the millennium, the FX market was a "plain vanilla" OTC market, with trading dominated by major dealers. While still retaining its OTC structure, a multitude of other venues and providers has emerged since then (see eg Chaboud et al (2022)).  For three decades, two electronic brokers, Reuters (now Refinitiv) Matching and Electronic Broking Services (EBS) Market, have been especially important for the inter-dealer spot market. Often referred to as the "primary venues", they are organised as central limit order books (CLOBs). They have been the main sources of reference prices for the entire spot market.

For three decades, two electronic brokers, Reuters (now Refinitiv) Matching and Electronic Broking Services (EBS) Market, have been especially important for the inter-dealer spot market. Often referred to as the "primary venues", they are organised as central limit order books (CLOBs). They have been the main sources of reference prices for the entire spot market.  But there are also more than 30 secondary venues in the dealer-customer market segment, which has grown strongly in recent years, especially when compared with primary market activity (Graph B1). Customers can also trade directly with more than 20 dealers via proprietary single-dealer platforms (SDPs) or obtain direct prices streams from more than a dozen PTFs.

But there are also more than 30 secondary venues in the dealer-customer market segment, which has grown strongly in recent years, especially when compared with primary market activity (Graph B1). Customers can also trade directly with more than 20 dealers via proprietary single-dealer platforms (SDPs) or obtain direct prices streams from more than a dozen PTFs.

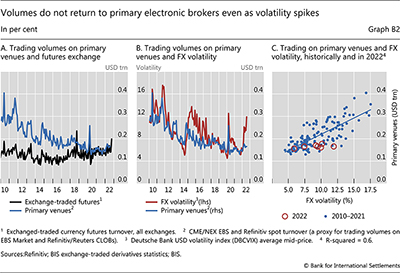

حجم معاملات در سالن های اصلی بیش از یک دهه در حال کاهش است (نمودار B2 ، پانل A). One reason is more intealisation. Another is that dealers were weary of adverse selection by PTFs engaging in high-frequency trading strategies (HFTs) after PTFs gained access to these venues in mid-2000s. In an attempt to insulate bank dealers from what were perceived as "toxic" HFT strategies, primary venues have subsequently introduced "speed bumps" to level the playing field. A third reason is the greater use of execution algorithms that help users, including dealers, to slice orders into smaller pieces and to distribute these efficiently across different venues. In 2020, execution algorithms were estimated to account for 10 20% of global FX spot trading (Markets Committee (2020)).  Last, PTFs often hedge the risk arising from liquidity provision to customers using futures rather than going to the primary venues. In part for this reason, futures markets have emerged as another locus for price discovery in currency markets alongside the primary venues (Chaboud et al (2021)).

Last, PTFs often hedge the risk arising from liquidity provision to customers using futures rather than going to the primary venues. In part for this reason, futures markets have emerged as another locus for price discovery in currency markets alongside the primary venues (Chaboud et al (2021)).

علیرغم روند نزولی آنها ، حجم در سالن های اولیه به طور معمول با نوسانات پرش کرده است اما امسال چنین نیست. برخی از حجم معاملات بین دلاری به طور معمول در شرایط بی ثبات به مکانهای اصلی بازگردانده شده اند (مور و همکاران (2016)) ، < SPAN> فروشنده فروشنده و معاملات بین دلاری در یک بازار پراکنده so that volumes rose as volatility increased (Graph B2, panels B and C). After an initial rise of trading on primary venues in early 2022, trading volumes remained flat as volatility continued to rise. This divergence may reflect several factors, including stagnating customer volumes, some decline in PTF activity, including on primary venues, higher intealisation ratios, more risk management with related parties, and a greater share of direct electronic execution even among dealers.

so that volumes rose as volatility increased (Graph B2, panels B and C). After an initial rise of trading on primary venues in early 2022, trading volumes remained flat as volatility continued to rise. This divergence may reflect several factors, including stagnating customer volumes, some decline in PTF activity, including on primary venues, higher intealisation ratios, more risk management with related parties, and a greater share of direct electronic execution even among dealers.

The views expressed are those of the authors and do not necessarily reflect those of the Bank for Inteational Settlements. Markets Committee, "Monitoring fast-paced electronic markets", report submitted by a Study Group, Markets Committee Papers , no 10, 2018. A Chaboud, D Rime and V Sushko, "The foreign exchange market", in R Gurkaynak and J Wright (eds), The Research Handbook of Financial Markets , available on SSRN, 2022. The time series shown in the graph overstate the tuover on primary venues because the publicly available data from EBS (CME/NEX Group) and Refinitiv include volumes traded on some of their other platforms. Markets Committee, "FX execution algorithms and market functioning", report submitted by a Study Group, Markets Committee Papers, no 13, 2022. A Chaboud, A Dao and C Vega, "What makes HFT tick? Tick size changes and information advantage in a market with fast and slow traders", available on SSRN, 2021. A Moore, A Schrimpf and V Sushko, "Downsized FX markets: causes and implications", BIS Quarterly Review , December, 2016, pp 35 51.

ما را در سایت آموزش تحلیل گری دنبال می کنید

برچسب :

نویسنده : ملیکا زارعی

بازدید : 68