- آموزش امواج رابرت بالان الیوت

- cryptocurrency بعدی برای منفجر شدن در سال 2022

- با افزایش سهم لوکس ، براساس آخرین داده های قیمت معاملات Kelley Blue Book ، قیمت های جدید در ماه نوامبر رکورد بالایی دارد

- FP Markets Account Demo: چگونه می توان از آن با تجارت استفاده کرد؟- یک آموزش سریع

- سبد سرمایه گذاری خود را بسازید

- 15 قانون معاملاتی ویکتور اسپراندو برای جلوگیری از اشتباه و دستیابی به بازدهی چشمگیر

- نحوه خرید سهام Google: سرمایه گذاری در سهام غول فناوری

- رالی بزرگ Smallcap. 5 رهبر و عقب مانده برتر.

- پنج اشتباه بزرگ از سرمایه گذاران "Do-It-Yourour"

- مسیرهای عصبی

آخرین مطالب

امکانات وب

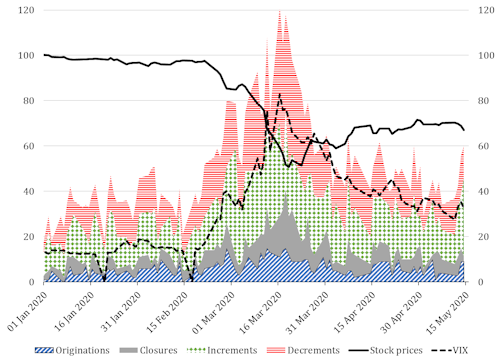

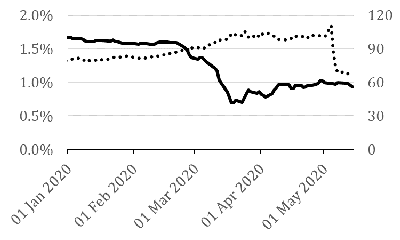

بحران Covid باعث واکنش بی سابقه ای از بازارهای سهام شده است. در آب و هوایی از وحشت گسترده ، این آموزنده است که به رفتار عوامل پیشرفته بازار مانند فروشندگان کوتاه نگاه کنیم. در اینجا ، هدف ما تجزیه و تحلیل مواضع فاش شده فروشندگان کوتاه در طول بحران Covid است. ما علاقه مند به درک این موضوع هستیم که آیا فروشندگان کوتاه پیش بینی شیوع همه گیر را پیش بینی کرده اند و آیا با سوار شدن به سقوط در بازار که در نتیجه می توانند سود کسب کنند. فروشندگان کوتاه پس زمینه اغلب توسط تنظیم کننده ها و رسانه ها مورد بررسی قرار گرفته اند زیرا می توانند از بازار در حال سقوط سود ببرند. نگرانی هایی که فروشندگان کوتاه می توانند فشار قیمت رو به پایین را افزایش دهند و بحران های تشدید کننده را افزایش دهند ، باعث شده تنظیم کننده ها در سراسر جهان در سال 2008 ممنوعیت فروش کوتاه را ممنوع کنند (Beber and Pagano ، 2013). تا حدودی ، این اتفاق در مورد شیوع اخیر COVID نیز رخ داده است. در تاریخ 12 مارس ، اداره بازارهای مالی ایتالیا ، Consob ، فروش کوتاه را در 85 سهام معامله شده در بورس ایتالیا ممنوع اعلام کرد. اخیراً ، به دنبال قوانین گسترده اتحادیه اروپا ، FCA تصمیم گرفت آستانه افشای فروش کوتاه را محکم کند و کوتاه تر آن را به طور موثری دشوارتر می کند. علیرغم این نگرانی ها ، تحقیقات نشان داده است که فروشندگان کوتاه عمدتاً با اطلاعات برتر تجارت می کنند ، که اغلب از مواضع متضاد حمایت می کنند (Boehmer and Wu ، 2013. ؛ Dechow et al. ، 2001). مطالعات نشان داده است که فروشندگان کوتاه می توانند اعلامیه های ناامید کننده درآمد را پیش بینی کنند (کریستوف و همکاران ، 2004) ، بازده منفی در بازار (لینچ و همکاران ، 2013) و همبستگی های تحقق یافته آینده (Geraci و همکاران 2020). داده ها ما افشای موقعیت فروش کوتاه را از وب سایت FCA جمع آوری کردیم. این موقعیت های کوتاه بزرگ ، خالص از موقعیت های مشتق طولانی و تنظیم شده ، در برابر سهام ذکر شده در بورس اوراق بهادار لندن است. به دنبال مقررات اتحادیه اروپا N. 236/2012 تصویب شده در نوامبر 2012 ، فروشندگان کوتاه موظفند موقعیت های کوتاه بزرگی را به تنظیم کننده ملی فاش کنند (در انگلستان ، این FCA است). این قانون مربوط به هر نهاد مالی است که بیش از 0. 5 ٪ از سرمایه بازار یک شرکت ذکر شده را کوتاه می کند. در میان سهام فاش شده توسط فروشندگان کوتاه ، ما تجزیه و تحلیل خود را در مورد سهام سهام عادی متمرکز کردیم و محل تجارت اولیه آنها LSE بود. برای این نمونه از 475 سهام ، ما داده های قیمت را از تامپسون رویترز ایکون جمع آوری می کنیم. تجزیه و تحلیل شکل 1 تعداد افشای روزانه منتشر شده در وب سایت FCA از ابتدای ژانویه را نشان می دهد. هر افشای می تواند به عنوان منشأ ، بسته شدن ، افزایش ، طبقه بندی شود Figure 1. Short selling disclosure and price level. Note: The figure presents the number of short selling position disclosures classified by type: originations (backward diagonal hatching - blue), closures (full - grey), increments (diamond - green), decrements (horizontal - red); the CBOE VIX (dashed), and the (equally weighted) average price level of the stocks in the sample (bold), with base period 2 Jan 2020. Short positions disclosures are from the FCA website, prices and CBOE VIX are from Thompson Reuters EIKON. All prices are in USD. The number of disclosed short positions peaked around the 18th of March. This represented a pivotal date for the Covid crisis in the UK, as on this day the govement announced closures of all schools from the following Friday, 20th of March. The decision was necessary because the virus was advancing faster than expected. As shown in Figure 1, this coincided with the peak in global volatility, indicated by the VIX, and the trough in stock prices. To obtain a more comprehensive view, the number of disclosures should be analysed jointly with the size of short positions. Figure 2 presents the short volume and short interest for the stocks in our sample, constructed using the disclosed positions. Short volume is the total capital (in USD millions) of open short positions, whereas short interest is the percentage of market capital shorted at a given period. During the Covid crisis, short volume fell abruptly. On the 21th of February, as Italy unveiled its first cases of Corona virus, open short positions accounted for almost $16 billion. In just over a month, the value of short positions halved. The decrease in short volume was mostly due to the concomitant price fall of stocks. During this same period, for the 475 stocks in our sample, the level of short interest remained relatively constant, which means that the average number of shares shorted was mostly the same. If anything, short sellers slightly decreased their positions after mid-March, when the average capital short sold fell to 0.63% compared to 0.67%, the level observed during the first part of the sample.

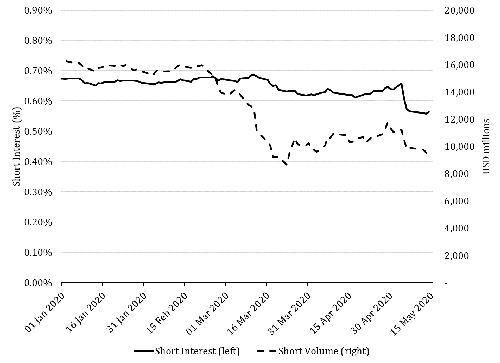

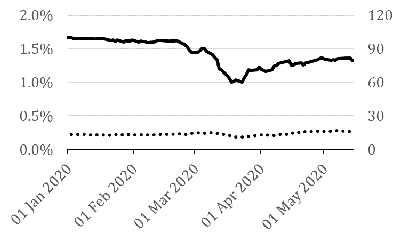

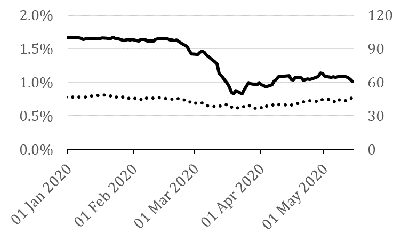

Figure 1. Short selling disclosure and price level. Note: The figure presents the number of short selling position disclosures classified by type: originations (backward diagonal hatching - blue), closures (full - grey), increments (diamond - green), decrements (horizontal - red); the CBOE VIX (dashed), and the (equally weighted) average price level of the stocks in the sample (bold), with base period 2 Jan 2020. Short positions disclosures are from the FCA website, prices and CBOE VIX are from Thompson Reuters EIKON. All prices are in USD. The number of disclosed short positions peaked around the 18th of March. This represented a pivotal date for the Covid crisis in the UK, as on this day the govement announced closures of all schools from the following Friday, 20th of March. The decision was necessary because the virus was advancing faster than expected. As shown in Figure 1, this coincided with the peak in global volatility, indicated by the VIX, and the trough in stock prices. To obtain a more comprehensive view, the number of disclosures should be analysed jointly with the size of short positions. Figure 2 presents the short volume and short interest for the stocks in our sample, constructed using the disclosed positions. Short volume is the total capital (in USD millions) of open short positions, whereas short interest is the percentage of market capital shorted at a given period. During the Covid crisis, short volume fell abruptly. On the 21th of February, as Italy unveiled its first cases of Corona virus, open short positions accounted for almost $16 billion. In just over a month, the value of short positions halved. The decrease in short volume was mostly due to the concomitant price fall of stocks. During this same period, for the 475 stocks in our sample, the level of short interest remained relatively constant, which means that the average number of shares shorted was mostly the same. If anything, short sellers slightly decreased their positions after mid-March, when the average capital short sold fell to 0.63% compared to 0.67%, the level observed during the first part of the sample.  Figure 2. Short interest and short volume. Note: The Figure shows the short interest (bold, left axis), which is the percentage of market capital short sold, and the short volume (dashed, right axis), the total value, in USD millions, of short positions. Short positions disclosures are from the FCA website, prices and shares outstanding are from Thompson Reuters EIKON. All prices are in USD. As shown in Figure 1, during the Covid outbreak, short sellers increased the number of disclosures submitted to the FCA. These disclosed short positions were not taken by the same short sellers. Rather, as depicted in Figure 3, the number of short sellers disclosing their positions increased during the crisis. This was coupled with an increase in the number of stocks short sold, indicating that short sellers enlarged the range of stocks they were dealing. Not all stocks were shorted equally. The disclosure data reveals that short sellers focused on some stocks more than others. We categorised stocks according to their Thompson Reuters Business Classification and computed the short interest for each sector. Figure 4 indicates that, over the crisis, consumer cyclicals had the largest increase in short interest. These are stocks that rely heavily on cyclical sectors, such as the automotive industry, housing, entertainment and retail, which were heavily hit by the Covid crisis. In comparison, short interest of non-cyclical stocks remained almost unmoved. Notice here that the increase in short interest of consumer cyclical stocks did not anticipate the price downfall, but rather was concomitant with it. This is in line with the finding that short sellers wait for prices to decline prior to start shorting, as it is costly to sustain an unprofitable short position for long (Curtis and Farghar, 2014).

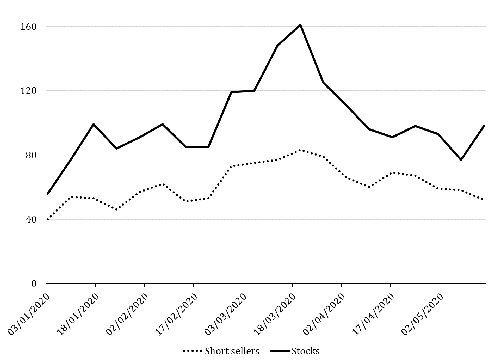

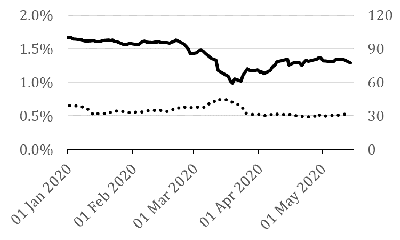

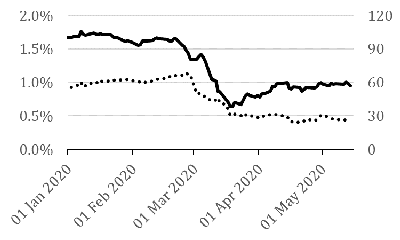

Figure 2. Short interest and short volume. Note: The Figure shows the short interest (bold, left axis), which is the percentage of market capital short sold, and the short volume (dashed, right axis), the total value, in USD millions, of short positions. Short positions disclosures are from the FCA website, prices and shares outstanding are from Thompson Reuters EIKON. All prices are in USD. As shown in Figure 1, during the Covid outbreak, short sellers increased the number of disclosures submitted to the FCA. These disclosed short positions were not taken by the same short sellers. Rather, as depicted in Figure 3, the number of short sellers disclosing their positions increased during the crisis. This was coupled with an increase in the number of stocks short sold, indicating that short sellers enlarged the range of stocks they were dealing. Not all stocks were shorted equally. The disclosure data reveals that short sellers focused on some stocks more than others. We categorised stocks according to their Thompson Reuters Business Classification and computed the short interest for each sector. Figure 4 indicates that, over the crisis, consumer cyclicals had the largest increase in short interest. These are stocks that rely heavily on cyclical sectors, such as the automotive industry, housing, entertainment and retail, which were heavily hit by the Covid crisis. In comparison, short interest of non-cyclical stocks remained almost unmoved. Notice here that the increase in short interest of consumer cyclical stocks did not anticipate the price downfall, but rather was concomitant with it. This is in line with the finding that short sellers wait for prices to decline prior to start shorting, as it is costly to sustain an unprofitable short position for long (Curtis and Farghar, 2014).  Figure 3 : Weekly number of short sellers and stocks involved in short position disclosures. Note: The figure shows the weekly number of different short sellers disclosing positions (dashed), and the weekly number of different stocks dealt by these short sellers (bold). Short positions disclosures are from the FCA website. Short sellers are not only known for trading on price downfalls. Decreases in their positions can also anticipate price surges (Boehmer et al., 2018). This seems to be the case for stocks in the basic materials and energy sectors in our sample---short sellers initially increased their positions and then successively decreased them after the peak of the crisis, prior to price rebounds. Among the stocks with the lowest short interest, were those of the healthcare sector. Throughout the sample period, on average only 0.09% of these stock’s capital was shorted, with a daily maximum of 0.18%. This was much less than what was observed for consumer cyclical and industrial stocks. Financials were also avoided by short sellers during the recent Covid crisis. This might be because bank stocks and other financials are often under the eye of regulators and this might dissuade short sellers from openly shorting them (Geraci et al. 2018). Conclusion Overall, short sellers do not seem to have predicted the sharp stock market declines caused by the Covid crisis. They increased their short positions against heavily hit consumer cyclicals as the crisis unfolded. On the other hand, disclosed shorts show that short sellers decreased their exposure to basic materials and energy stocks, perhaps indicating that they do not believe price declines in these sectors to be sustainable for long.

Figure 3 : Weekly number of short sellers and stocks involved in short position disclosures. Note: The figure shows the weekly number of different short sellers disclosing positions (dashed), and the weekly number of different stocks dealt by these short sellers (bold). Short positions disclosures are from the FCA website. Short sellers are not only known for trading on price downfalls. Decreases in their positions can also anticipate price surges (Boehmer et al., 2018). This seems to be the case for stocks in the basic materials and energy sectors in our sample---short sellers initially increased their positions and then successively decreased them after the peak of the crisis, prior to price rebounds. Among the stocks with the lowest short interest, were those of the healthcare sector. Throughout the sample period, on average only 0.09% of these stock’s capital was shorted, with a daily maximum of 0.18%. This was much less than what was observed for consumer cyclical and industrial stocks. Financials were also avoided by short sellers during the recent Covid crisis. This might be because bank stocks and other financials are often under the eye of regulators and this might dissuade short sellers from openly shorting them (Geraci et al. 2018). Conclusion Overall, short sellers do not seem to have predicted the sharp stock market declines caused by the Covid crisis. They increased their short positions against heavily hit consumer cyclicals as the crisis unfolded. On the other hand, disclosed shorts show that short sellers decreased their exposure to basic materials and energy stocks, perhaps indicating that they do not believe price declines in these sectors to be sustainable for long.

یا کاهشمنشأ اولین افشاگری است که وقتی موقعیت آنها از آستانه 5 ٪ عبور می کند ، توسط یک فروشنده کوتاه انجام می شود. به طور مشابه ، بسته شدن آخرین افشای یک موقعیت کوتاه است و هنگام تصویب آستانه از بالا رخ می دهد. افشای باقیمانده را می توان به عنوان افزایش موقعیت یا کاهش موقعیت طبقه بندی کرد. از اواسط ماه فوریه ، تعداد افشای فروش کوتاه در هر چهار دسته افزایش یافته است که نشانگر افزایش فعالیت توسط فروشندگان کوتاه است. از اواسط فوریه تا اوایل مارس ، در مراحل اولیه شیوع Covid در اروپا ، تعداد افزایش موقعیت به سرعت افزایش یافت. با این حال ، از ماه مارس ، به عنوان قیمت سهام (خط جسورانه) همچنان در سراسر هیئت مدیره قرار گرفت ، ما همچنین شاهد افزایش سریع تعداد کاهش و بسته شدن موقعیت روزانه بودیم. در مقایسه ، افزایش منشاء یعنی موقعیت های کوتاه جدید ، بسیار کوچکتر بود.

مواد اصلی

حلقوی مصرف کننده

غیر چرخه مصرف کننده

انرژی

مالی

مراقبت های بهداشتی

صنعت

فن آوری

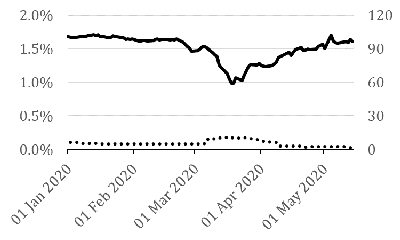

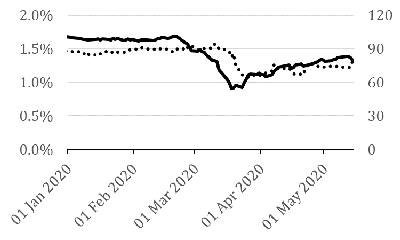

شکل 4: علاقه کوتاه سهام برای بخش های مختلف اقتصاد. توجه: شکل نشان می دهد علاقه کوتاه (متراکم ، محور چپ) ، که درصد سرمایه گذاری در بازار کوتاه فروخته شده و سطح قیمت سهام به همان اندازه وزن (محور جسورانه ، راست) برای سهام بخش های مختلف ، با دوره پایه 2 ژانویه است. 2020. سهام با توجه به طبقه بندی تجاری تامپسون رویترز طبقه بندی می شوند. افشای موقعیت های کوتاه از وب سایت FCA است ، قیمت ها و سهام برجسته از تامپسون رویترز ایکون است. تمام قیمت ها به دلار است. منابع Beber ، A. & Pagano ، M. (2013). ممنوعیت های کوتاه فروش در سراسر جهان و شواهدی از بحران. مجله مالی ، 58: 344—381. Boehmer ، E. & Wu ، J. J. (2013). فروش کوتاه و روند کشف قیمت. مرور مطالعات مالی ، 26: 287—322. Boehmer ، E. ؛Duong ، T. X. & Huszaár ، Z. R. (2018). معاملات کوتاهمجله تجزیه و تحلیل مالی و کمی ، 53: 723—348. کریستوف ، س. ه. ؛Ferri ، M. G. & Angel ، J. J. (2004). فروش کوتاه قبل از اعلامیه های درآمد. مجله مالی ، 59: 1845 - 1875. Curtis ، A. & Fargher ، N. L. (2014). آیا فروش کوتاه باعث کاهش قیمت کاهش می یابد یا سهام را با ارزش های اساسی خود تراز می کند؟علوم مدیریت ، 60: 2324—2340. DeChow ، P. M. ؛هاتون ، A. ص. ؛Meulbroek ، L. & Sloan ، R. G. (2001). فروشندگان کوتاه ، تجزیه و تحلیل اساسی و بازده سهام مجله اقتصاد مالی ، 61: 77—106. Geraci ، M. v. ؛Garbaravicius ، T. ، Veredas ، D. (2018). فروش کوتاه در رویدادهای شدید. مجله ثبات مالی ، 39: 90—103. لینچ ، ا. نیکولیک ، ب. ؛Yan ، X. & Yu ، H. (2013). کل فروش کوتاه ، مشترک بودن و بازده بورس سهام. مجله بازارهای مالی ، 17: 199—229.

آموزش تحلیل گری...

ما را در سایت آموزش تحلیل گری دنبال می کنید

برچسب :

نویسنده : ملیکا زارعی

بازدید : 32